Issue: May 29, 2018

New Audit Rules: Part 1 – Who Can Opt Out?

There are changes coming, effective this tax year, that require all entities taxed as partnerships to contemplate many issues that they haven’t needed to in the past. In this multi-part series, we will outline several provisions in the new IRS audit rules that impact these entities. These changes directly affect both general and limited partnerships as well as limited liability companies that are taxed as partnerships.

The new rules were enacted by Congress in the Bipartisan Budget Act of 2015 (“BBA”) and are sometimes referred to as the BBA audit rules. These rules completely replace the old partnership audit rules. Under the prior audit rules, any IRS audit adjustments were made at the partner level (with each partner having to pay his share of any underpayment); but the new rules impose liability – under the default rule – at the partnership level. The rules are much more complex and perhaps draconian than the old rules since they can impose liability even on partners who were not members of the partnership or the LLC for the year being audited!

Before plowing through the new rules, the first question to ask is: Can I get my entity excluded from these new rules and what do I have to do to get excluded?

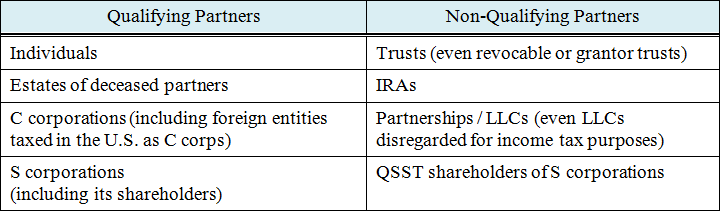

The good news is that BBA “small” partnerships can opt out; the bad news is that opting out may be more trouble than it is worth, and might not even be available. Generally speaking, a BBA small partnership is one that has 100 or fewer partners. But, don’t stop reading just because your LLC or partnership has fewer than 100 members. To be able to opt out, each and every partner or member must be a qualifying partner.

Assuming all partners are qualified, the partnership has to make an annual election to “opt out” of the BBA audit rules. In order to do so, it must make the election on the partnership tax return and each partner must receive notice of the election in writing. If the election is not timely made annually, or if a partnership interest passes to a non-qualifying partner, the opt-out will not be effective for that tax year.

Thus, even if you think that you might want to opt-out of the BBA audit rules, prudence dictates that the BBA audit rules be addressed in your partnership agreement or LLC operating agreement. For example, you might want to mandate that only qualifying partners can ever hold an interest. But what if you already have a non-qualifying member?

We’ve assembled a team of our business attorneys to help our clients evaluate these new rules and decide how to address them in their partnership agreement or LLC operating agreement. If you’d like to have us evaluate your situation, let us know at New_IRS_Audit_Rules@gblaw.com. We look forward to hearing from you.

You can read the next alert of the series online here: Part 2 – The Partnership Prepresentative.

If you’re looking for the third part of the series, you can read about it here: Part 3 – Who Pays the Tax.

Download the full Legal Alert about part one of the new audit rules.